How Crypto Tax Canada Affects You: Reporting, Losses & Tips

Crypto Tax Canada, Explained: Key Tax Rules To Know

Key Takeaways:

- In Canada, 50% of crypto capital gains are taxable, while 100% of business income from crypto is taxed.

- Accurate transaction records are required for compliance, with gains or losses reported on the appropriate forms.

- To minimize crypto tax liability, Canadians can invest in a TFSA for tax-free growth or an RRSP to defer taxes until retirement

Cryptocurrency has become a widely used asset globally. Some countries, like El Salvador, have officially adopted it, while others, such as China, maintain a hostile stance towards these digital assets. Countries like India and Pakistan have not accepted crypto and have instead imposed hefty taxes.

As a result, many investors face tax obligations on their crypto earnings. It is crucial for investors to report all earnings to avoid potential legal issues. Since crypto is a relatively new asset class, the tax process may seem complex to some.

The government provides detailed guidelines for calculating taxable events. In Canada, the government classifies crypto as a commodity for tax purposes. The Canada Revenue Agency (CRA) offers clear rules for digital currency transactions.

We'll break everything down in this guide, so you can understand how crypto tax in Canada works.

Is Cryptocurrency Taxed in Canada?

Canada became the first country to approve a Bitcoin exchange-traded fund (ETF), allowing traders to trade on the Toronto Stock Exchange.

Cryptocurrencies are legal in Canada but do not qualify as legal tender. As a result, all trading platforms, individuals, and businesses must adhere to the established rules and regulations. In 2014, the Canada Revenue Agency (CRA) classified cryptocurrencies, such as Bitcoin, as commodities for tax purposes.

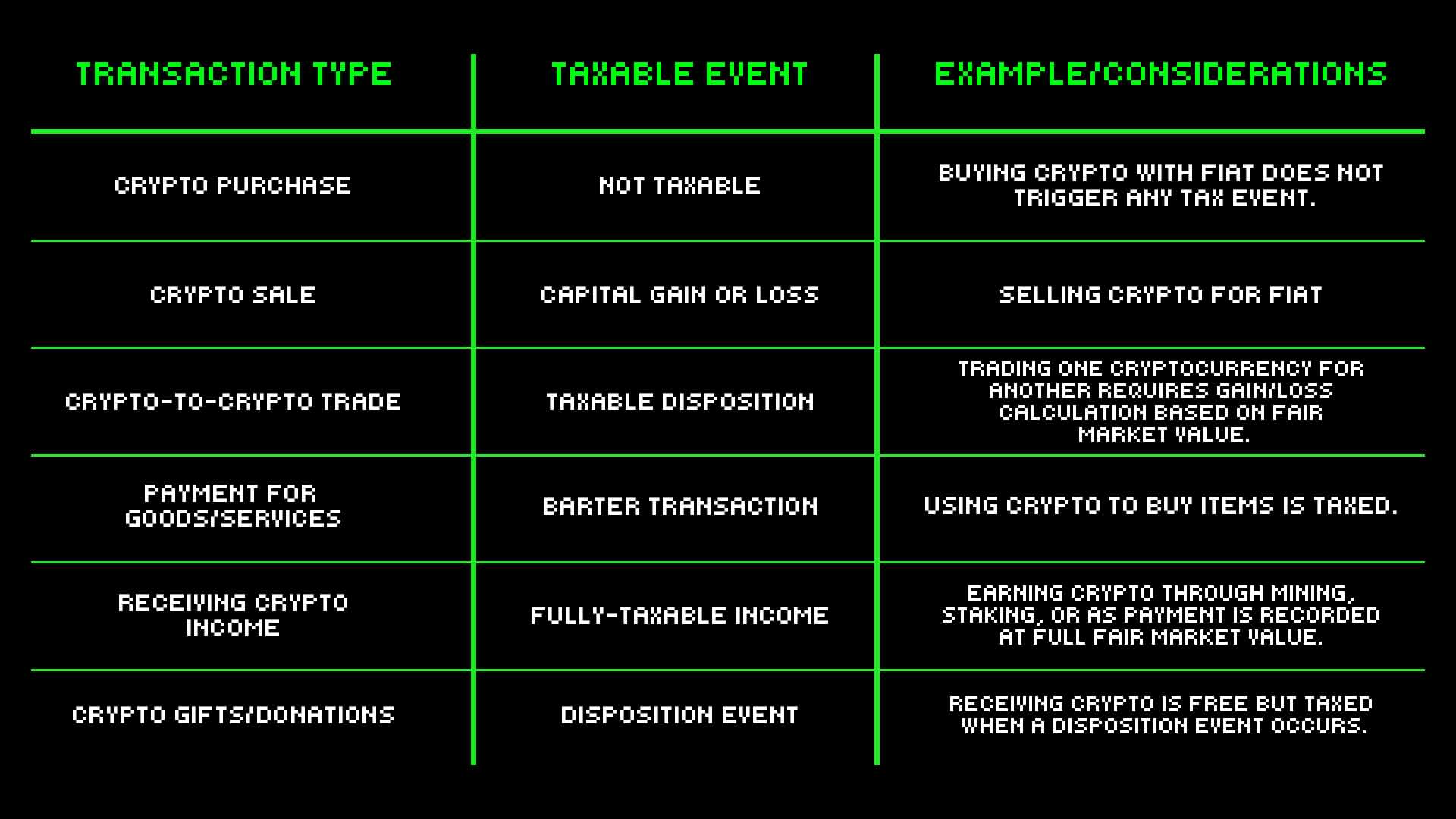

Here's an overview of taxable and tax-free events in Canada:

In 2017, as cryptocurrency regulations became clearer, the Canadian Securities Administrators (CSA) released a comprehensive set of guidelines. These guidelines classified certain types of crypto tokens as securities, including NFTs, utility tokens, and digital assets under securities law.

Below is a table presenting the federal income tax bands for 2024 and 2025:

| Tax Rate | Income (2024) | Income (2025) |

|---|---|---|

| 15% | $55,867 or less | $57,375 or less |

| 20.5% | $55,867 - $111,733 | $57,375.01 - $114,750 |

| 26% | $111,733 - $173,205 | $114,751 - $177,882 |

| 29% | $173,205 - $246,752 | $177,883 - $253,414 |

| 33% | $246,752+ | $253,414.01+ |

Canada considers 50% of capital gains and 100% of business income from cryptocurrency taxable. However, day traders are subject to 100% tax obligations. The tax is based on specific transaction types and the amount involved.

Below is an example of such events or transactions to determine the value of cryptocurrency assets subject to tax.

| Acquisition | Disposition |

|---|---|

| Purchase | Sale |

| Exchange with another crypto | Exchange with another crypto |

| Receiving crypto for goods or services | Using crypto for goods or services |

| Receiving as a gift or donation | Gifting or donating crypto |

| Winning from gambling | Wagering in gambling |

| Earning from mining or staking | Not applicable |

The CRA calculates tax based on the fair value of cryptocurrency assets for reporting purposes.

Tax-Free Crypto

- Moving crypto between wallets

- Holding crypto

- Buying crypto with fiat

- Creating a DAO (Decentralized Autonomous Organization)

- Being gifted crypto

Capital Gains Tax

What is Capital Gains Tax?

Capital gains tax is the tax you pay on the profit made from selling your assets. In Canada, capital gains are considered taxable income. If you sell cryptocurrencies, vacation property, NFTs, or stocks, the profit you make will be classified as a capital gain. For crypto profits in Canada, you are required to pay capital gains tax on 50% of the profit.

The total tax you owe depends on your overall profit and your place of residence. A proposal to increase the tax on capital gains was introduced but has been deferred until 2026.

In Canada, the first $15,705 you earn in income is tax-free for the 2024 financial year, or $16,129 for the 2025 financial year.

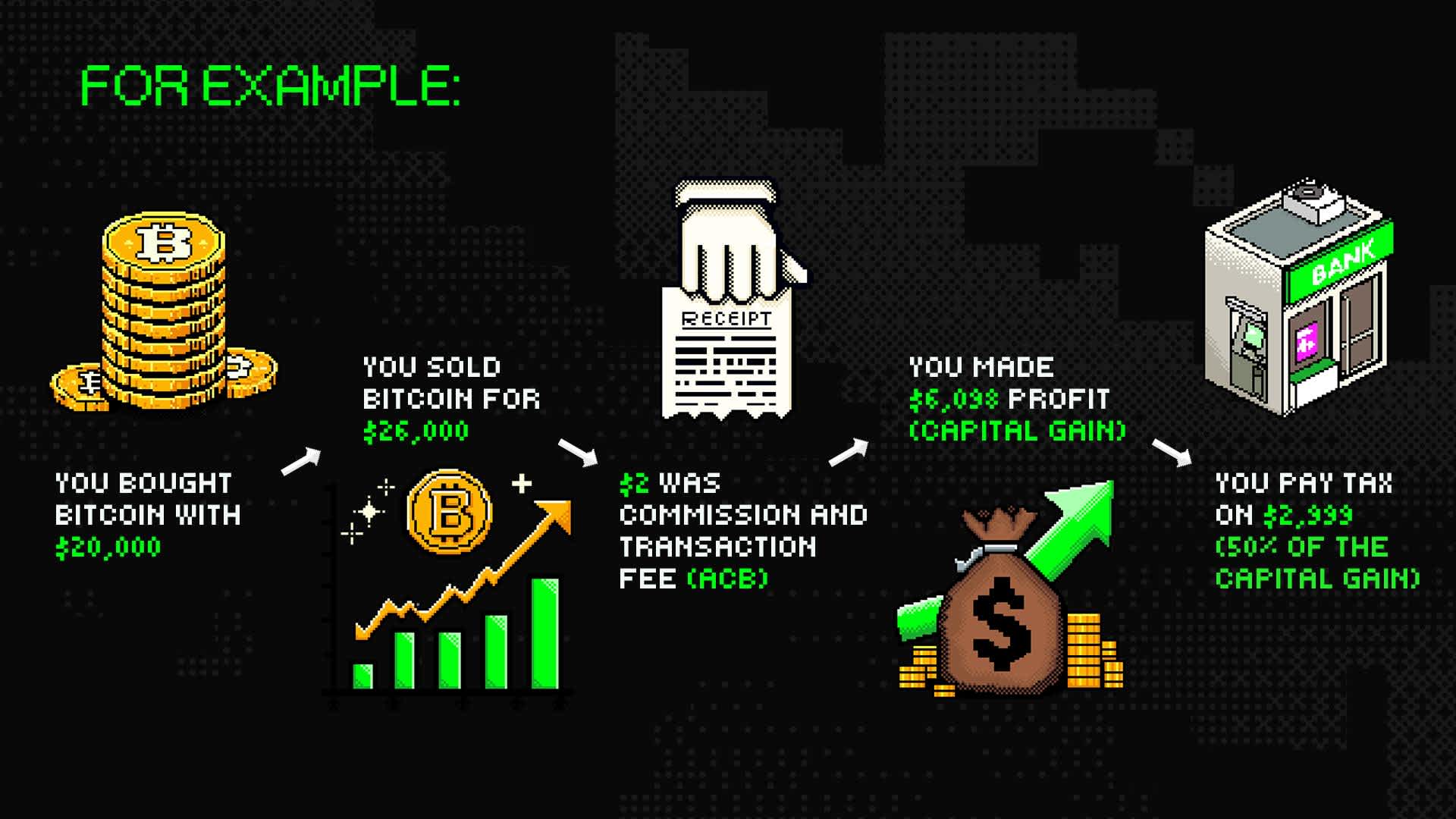

How to Calculate Capital Gains

To calculate crypto capital gains tax:

- Start with the sale price (or value at the time of disposal).

- Subtract the purchase price, also known as the adjusted cost basic (ACB)

- The result is your capital gain or loss. If negative, it's a capital loss. If positive, it's a capital gain.

Here's an example:

The ACB is the total cost paid for acquiring an asset, including the purchase price, fees, and commissions. Detailed records of all transactions, including dates, values, and costs, should be maintained.

Business Income Tax

What Falls Under Business Activities?

Crypto-related activities in Canada may be considered business activities depending on factors like trading frequency, the level of organization, and the intent behind transactions.

If you actively buy and sell cryptocurrencies, or earn from staking, mining, or other crypto-related services, these activities can be classified as business activities. Business income from cryptocurrency is taxed at the same rate as other business income in Canada.

Business Income Tax Implications

When crypto activities qualify as business income, the full amount of the profit is subject to taxation. Unlike capital gains, where only 50% of the profit is taxable, business income is taxed entirely. This income from cryptocurrency must be reported annually on the income tax return (T1).

Because you're actively day trading, this profit is considered business income. Therefore, you must report the full $40,000 as taxable income on your tax return. The CRA may also require the taxpayer to file additional forms, such as the T2125 Statement of Business or Professional Activities.

Tax Planning Strategies

Tax-Free Savings Account

Under Canadian tax regulations, a Tax-Free Savings Account (TFSA) lets Canadians invest after-tax dollars without paying tax on capital gains or income earned within the account, provided they're eligible account holders.

While a TFSA does not permit account holders to directly hold cryptocurrencies, they can indirectly access these assets through crypto ETFs or trusts that track the performance of digital currencies.

With a TFSA, account holders can benefit from tax-free growth and tax-free withdrawals. This makes it a great option for long-term investing, since TFSA contributors can use their accounts to maximize savings in any tax year. Additionally, a TFSA can help lower taxable income.

However, the CRA may consider income earned from cryptocurrency investments within a TFSA as business income if the investments are made with the intent to profit. In such cases, this income must be reported on the annual income tax return.

Cryptocurrency Losses and Stolen Crypto

Crypto losses can reduce the overall capital gains tax and business income tax liability by offsetting capital gains. Any stolen or lost crypto assets are also treated as losses, and can help reduce overall crypto taxes.

Similarly, selling crypto at a loss reduces capital gains, thereby decreasing taxable capital gains. Unused losses can be carried forward or back to prior years, providing flexibility in tax planning.

Cryptocurrency losses can be used to offset capital gains from other investments, reducing the taxable income from other sources. If your cryptocurrencies were stolen and you have proper documentation to prove the theft, you can claim the losses to lower your tax liability. To report cryptocurrency taxes, it’s essential to maintain accurate records and timely report the losses as net capital loss for compliance.

Reporting and Compliance

Compliance and Record-Keeping

The CRA requires taxpayers to maintain accurate records of their cryptocurrency transactions. These records should include the date, time, and amount of each transaction, along with the type of transaction (buy, sell, trade, etc.).

Crypto transactions made with the intention of profiting through trading are considered business income and subject to capital gains tax. Taxpayers must also keep track of their cryptocurrency holdings, including the fair market value of each holding.

Specific Crypto Transactions

Buying and Selling Cryptocurrency

Buying crypto with fiat currency like CAD is tax-free.

Here are some factors you should keep in mind when buying and selling crypto.

- Buying and selling cryptocurrency is subject to capital gains tax. However, buying cryptocurrencies with EUR, Canadian dollars, or US dollars is tax-free.

- Tax implications, such as capital gains tax or business income tax, apply once you realize your gains.

- Transferring cryptocurrencies between your own wallets is not taxed in Canada.

- Swapping cryptocurrencies (e.g., buying crypto with other crypto) is taxed in Canada, as it is treated as crypto trading.

The Canada cost basis method is used to calculate capital gains or losses for cryptocurrency tax reporting. Capital gain is determined by subtracting the adjusted cost basis (ACB) from the fair market value of the cryptocurrency at the time of sale.

Mining and Staking

Both crypto mining and staking are considered business crypto transactions, and are subject to tax liability. Whether these activities are intended to make a profit or conducted as a hobby, if crypto mining results in profit and capital gains, it will be taxed when disposed of.

While reporting capital gain or loss from mining and staking, you can deduct the expenses like cost of hardware, electricity, and maintenance to lower your taxable income. Both mining and staking rewards are taxed based on their fair market value at the time of receipt and are considered income, which triggers income tax implications. The average cost basis method and adjusted cost basis method are applied to these gains when calculating overall tax liability.

NFTs and DeFi

NFTs and decentralized finance (DeFi) are treated as capital property, and capital gains tax applies to gains or losses calculated on disposition. However, creating a decentralized autonomous organization (DAO) is tax-free, much like crypto gifts.

Frequent buying and selling of NFTs may be considered a business activity, subjecting you to full income tax. DeFi activities, such as yield farming or liquidity mining, are generally taxed as ordinary income.

Audits and Penalties

Can I be Audited for Cryptocurrency in Canada?

Yes, the CRA can audit taxpayers for cryptocurrency transactions and may request additional information or documentation to verify tax reporting. It is advised to use only legal crypto exchanges and avoid Web3 wallets, as they are harder to track and maintain records.

Taxpayers in Canada may face penalties and fines for underreporting or misreporting cryptocurrency income or capital gains.

Filing Your Crypto Taxes

Cryptocurrencies are still relatively new and considered controversial in many countries. Governments began regulating cryptocurrencies in 2009 and are still working to refine their tax filing systems. It is essential to strike a balance between keeping digital assets unregulated and over-regulating cryptocurrencies, which could discourage investors.

However, in Canada, cryptocurrency taxes apply to all residents, and tax evasion is considered illegal. Canadians can file crypto taxes online by using a combination of crypto tax software.

Anyone in Canada can file crypto taxes in five simple steps based on their crypto income category:

- Gather all crypto transaction data.

- Calculate your gains and losses.

- Create a CRA-compliant tax report.

- Complete the required tax forms.

- File your return online via CRA 'My Account'.

Most crypto exchanges offer tools to help users download transaction activity reports with various filters. You can easily download taxable capital gains by selecting specific dates. Be sure to check federal and provincial income tax rates before filing your taxes. Always consult a tax professional to ensure compliance with Canadian tax laws.

FAQs

Q: How to avoid crypto taxes in Canada?

A: Capital gains tax regulations require all Canadian residents to pay tax on their reported crypto earnings. Avoiding crypto taxes in Canada is illegal and unethical. However, there are ways to minimize your crypto tax obligations:

Since both crypto capital gains tax and business income tax apply at the disposition of crypto assets, holding cryptocurrency for over a year can help you benefit from capital gains tax.

Q: Do you pay taxes on crypto before withdrawal?

A: No. You are not liable for tax when transferring or withdrawing your crypto from an exchange or between wallets. Taxes are only triggered when you dispose of the crypto by selling, trading, or using it to purchase goods or services.

Q: How much is crypto taxed in Canada?

A: For crypto investors, 50% of the capital gain is included in taxable income. If your crypto activities qualify as business activities, 100% of the profit is taxable. Professional (day) traders also pay tax on 100% of their profits.

Q: How much is crypto taxed?

A: The taxable portion varies depending on the activity. The tax liability changes based on your place of residence and the value of your digital assets. Taxes range from a minimum of 15% to a maximum of 33%, depending on your federal and provincial marginal tax rates.

Q: How is crypto taxed in Canada?

A: Cryptocurrency is treated as a commodity. When you dispose of it, the CRA determines whether the transaction results in a capital gain (with only 50% of the gain taxable) or business income (with 100% taxable). Your tax liability depends on the classification of the transaction.

Q: How to file crypto taxes in Canada?

A: Keep a record of all your crypto transactions, including dates, amounts, wallet addresses, and fees. Report crypto capital gains or losses on Schedule 3 of your tax return. For business income tax, use Form T2125 to report taxes based on fair market value.

Q: How much tax on crypto in Canada?

A: Cryptocurrency assets are taxed in Canada based on how your gains are classified. For capital gains, only 50% of the gain is taxable. For business income from crypto, the entire profit is taxable according to your marginal tax bracket, which can range from 15% to over 33% federally.